- Glossary

- What Is Gross Monthly Income?

- What Is Management?

- What Is A Problem Statement?

- What Is Annual Net Income?

- What Is A Letter Of Transmittal?

- What Is Attrition?

- What Does White Collar Mean?

- What Does Blue Collar Mean?

- What Is Efficiency Vs Effectiveness?

- What Is A Dislocated Worker?

- What Is Human Resource (HR)?

- Thank You Letter Scholarships

- What Is Constructive Criticism?

- What Is A Quarter Life Crisis?

- What Is Imposter Syndrome?

- What Is Notes Payable?

- Types Of Communication

- Economic Demand

- Cost Benefit Analysis

- Collective Bargaining

- Key Performance Indicators

- What Is Gender Bias In A Job Description?

- What Is The Hidden Job Market?

- What Is The Difference Between A Job Vs. A Career?

- What Is A Prorated Salary?

- W9 Vs. 1099

- Double Declining Balance Method

- Divergent Vs Convergent Thinking

- Budgeting Process

- Types Of Intelligence

- What Is Bargaining Power?

- What Is Operating Capital?

- Difference Between Margin Vs Markup

- Participative Leadership

- Autocratic Leadership

- Authoratarian Leadership

- Situational Leadership

- Difference Between Generalist Vs Specialist

- Strategic Leadership

- Competitive Strategies

- Equity Vs Equality

- What Is Marginalization?

- Colleague Vs Coworker

- What Is The Glass Ceiling?

- What Are Guilty Pleasures?

- Emotion Wheel

- Nepotism In The Workplace

- Sustainable Competitive Advantage

- Organizational Development

- Communication Styles

- Contingent Workers

- Passive Vs Non Passive Income

- Choose A Career

- Formulas

- APR Formula

- Total Variable Cost Formula

- How to Calculate Probability

- How To Find A Percentile

- How To Calculate Weighted Average

- What Is The Sample Mean?

- Hot To Calculate Growth Rate

- Hot To Calculate Inflation Rate

- How To Calculate Marginal Utility

- How To Average Percentages

- Calculate Debt To Asset Ratio

- How To Calculate Percent Yield

- Fixed Cost Formula

- How To Calculate Interest

- How To Calculate Earnings Per Share

- How To Calculate Retained Earnings

- How To Calculate Adjusted Gross Income

- How To Calculate Consumer Price Index

- How To Calculate Cost Of Goods Sold

- How To Calculate Correlation

- How To Calculate Confidence Interval

- How To Calculate Consumer Surplus

- How To Calculate Debt To Income Ratio

- How To Calculate Depreciation

- How To Calculate Elasticity Of Demand

- How To Calculate Equity

- How To Calculate Full Time Equivalent

- How To Calculate Gross Profit Percentage

- How To Calculate Margin Of Error

- How To Calculate Opportunity Cost

- How To Calculate Operating Cash Flow

- How To Calculate Operating Income

- How To Calculate Odds

- How To Calculate Percent Change

- How To Calculate Z Score

- Cost Of Capital Formula

- How To Calculate Time And A Half

- Types Of Variables

Find a Job You Really Want In

The economy is a diverse system laced with systems within systems. Such Inception-like layers make us appreciate the many different factors that are important to the economy. In some cases, these factors can affect the economy in meaningful ways due to their complex intertwined relationships.

For example, we say the economy is doing well when the highest possible amount of people and businesses can buy goods and services. When the opposite happens, we say the economy is doing poorly.

Demand is one of these interwoven factors that help us understand the economy’s peaks and troughs. Therefore, understanding demand is critical to successfully navigating the economy.

What Is Economic Demand?

Economic demand refers to the consumer’s willingness and ability to buy a certain amount of a good or service at a specific price. You can also think of demand as to whether or not a consumer can or will pay for a good or service.

Demand drives the economy. Businesses cater to consumers’ demand because, without such demand for the product or service, the businesses would fail. Therefore it is important for businesses to understand demand and, if possible, influence demand to their advantage. This is why as an employee, your job may depend on your understanding of demand.

Some positions, such as in market research and sales, are greatly affected by the demands of their clients and customers. A company’s decision to allocate resources considers the current or future demand of their good or service. To influence future demand, a company may roll out different marketing and sales strategies.

As the definition implies, demand relies on different characteristics of the consumer. To understand demand, you first need to understand the consumer. The willingness of a consumer to pay for a good or service comes from both internal and external reasons. These reasons are the determinants of demand.

What Are The Determinants Demand?

Determinants of demand are the factors that consumers either consciously or subconsciously consider when they decide whether or not to pay for a good or service. Sometimes their demand results from their willingness, while other times, it is a question of ability.

When we discuss specific determinants of demand, we must consider the phrase “ceteris paribus”, which means “all other things being equal.” This is the phrase economists use to reflect on the fact that determinants impact each other as much as demand.

So we will hypothetically assume that the other determinants won’t change when we discuss certain determinants such as:

-

Price. Price is the main determinant to focus on for many economists and businesses. The Law of Demand states that as prices rise, the quantity of demand falls. Consumers are less likely to pay for more of a good or service when the price increases.

This is why companies constantly set their price to optimal levels that don’t hurt demand while still providing a maximum profit.

-

Price of related or competitive goods/services. Much like the price of a good or service in question, the price of related goods and services can affect the consumer’s demand. If a competitor’s price falls, for example, then demand will shift away from the good in question towards the competitor.

-

Income. As income rises, consumers will buy more of a product. However, you must factor in marginal utility with this determinant because the product loses its usefulness as quantity increases. Consider when you buy a car. Generally, you will only buy as many cars as you need and spend any extra money somewhere else.

-

Tastes and preferences. The tastes and preferences of consumers are themselves determined by a variety of factors. Some are based on values, while others are based on fads and trends. Due to this, tastes and preferences are constantly monitored by businesses. Eco-friendly products are one example of businesses meeting this type of demand.

-

Expectations. Sometimes, consumers will base their demand on expectations of the future state of the market. If a consumer feels the price will increase over time, they will try to buy more before the change. This is especially true for goods and services that are limited in supply, such as plane tickets.

-

Number of competitive consumers. Demand rises when more competition exists between consumers. Consumers will pay more for a good or service if they are forced to outbid other consumers.

What Are the Types of Demand?

Demand can be broken up into several categories to clarify the relationship of the good or service to other goods and services. Some types of demand include:

-

Effective demand. Effective demand is the willingness or ability of a consumer to pay for goods at different prices. This is the demand that consumers are actually acting on in the market. Monitoring effective demand is one way to monitor the health of an economy.

-

Derived demand. Derived demand is a demand for a good or service affected by factors of production-related to the final product. Say there is a high demand for cars, then there will be a high demand for steel and other necessary resources.

-

Composite demand. Composite demand exists when there are multiple uses for a single product. These individual demands add up to create composite demand. Plastic is a good example of composite demand since plastic is used for so many different types of goods. As demand for plastic goods rises, the demand for plastic rises as well.

-

Joint demand Joint demand is the attached demand for complementary goods or services. These related goods will share a positive relationship where the increase of one demand increases the other. It is similar to effective demand except that joint demand refers to two independent goods or services such as ketchup and french fries.

Demand Schedule and Demand Curve

Now that we understand some of the determinants and types of demand, we should now consider how to organize this information. As we have seen, demand is the result of certain factors in the consumer’s needs and wants. Some of these factors can be measured, and in particular, economists and businesses focus on price and how it relates to quantity demanded.

Again, the Law of Demand states that all other factors being equal, as the price of a good or service increases, the quantity demanded will decrease. We can see this occur if we organize the change in price and the change in quantity demanded in a table called the demand schedule.

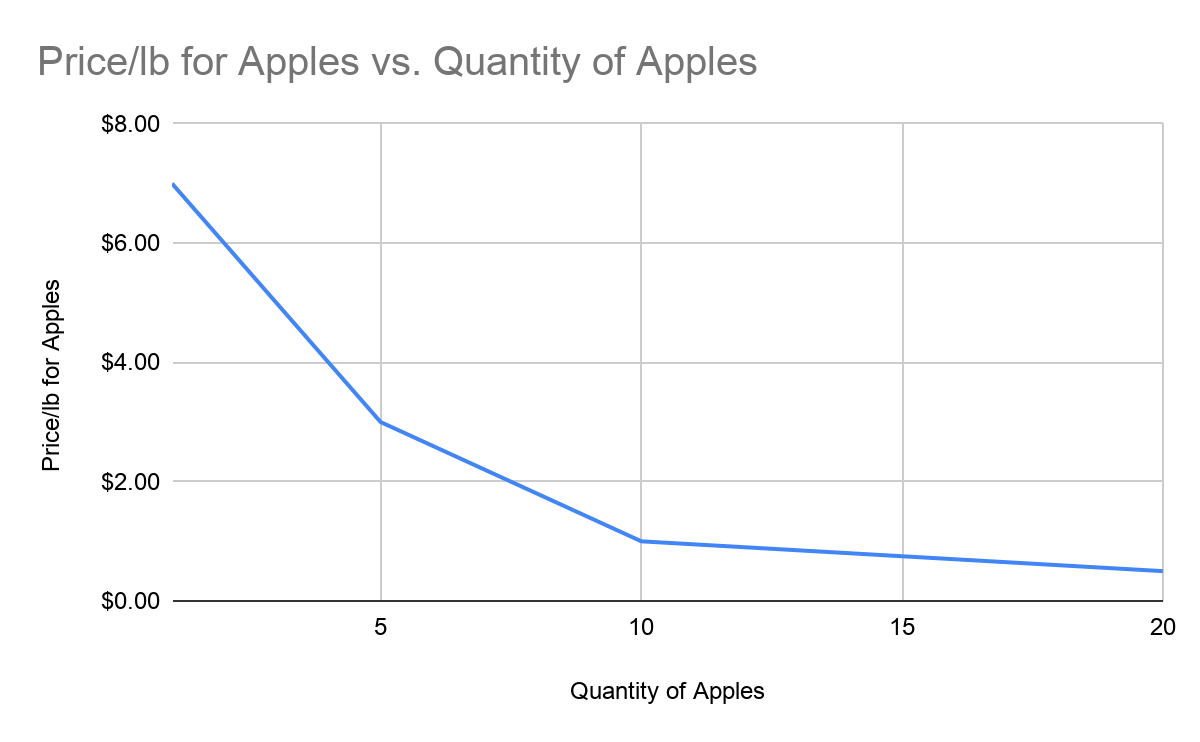

Imagine you run a business that sells apples by the pound. As you raise the price per pound, you can expect to see a drop in the quantity demanded by an individual customer. You track these changes, and your demand schedule looks like this:

| Price/lb for Apples | Quantity of Apples |

|---|---|

| $0.25 | 20 |

| $1.00 | 10 |

| $3.00 | 5 |

| $5.00 | 3 |

| $7.00 | 1 |

Economists like to input the information of a demanding schedule into a graph. The graphical representation is called the demand curve. The demand curve allows us to visually see how demand is affected by price and makes it easier for readers.

If we follow our apple business example, the demand curve of your business will look like this:

Note that in economics, the independent variable, price, is on the y-axis.

When we look at the graph, we can notice that the quantity demanded decreases significantly as the price changes. Due to this, we would say the demand for apples is elastic.

The elasticity of demand, or price elasticity of demand, is the degree to which a change in price affects the quantity demanded. Elastic demand means a change in price has a high impact on the quantity demanded.

If another determinant of demand changes, then we would see a shift in the demand curve and have to draw a new curve entirely.

For example, if the income of customers dropped, then we would see a decreased change in quantity demanded at all levels. The demand curve would then shift to the left.

Supply and Demand Curves

Demand is one important component that affects the economy. Another is supply.

In brief, supply is the total amount of a good or service businesses are able to provide. The relationship between supply and demand is a fundamental aspect of the economy. Where the consumer’s demand meets the supply of the producer, we find a market price for that good or service.

This is because the demand curve and supply curve have an inverse relationship. We know that as the price of a good or service increases, the quantity demanded decreases.

For a supply curve, as the price of a good increase, the supply of the quantity provided increases as well. This happens because businesses will want to maximize profits and sell as much as possible at the highest price possible.

Therefore most points along either curve will be out of sync with the other. At a low price, a consumer will demand a high amount of the good or service, but the producer will only provide a low quantity at the same price. A business can not expect to make much off a low price and will not produce to save money.

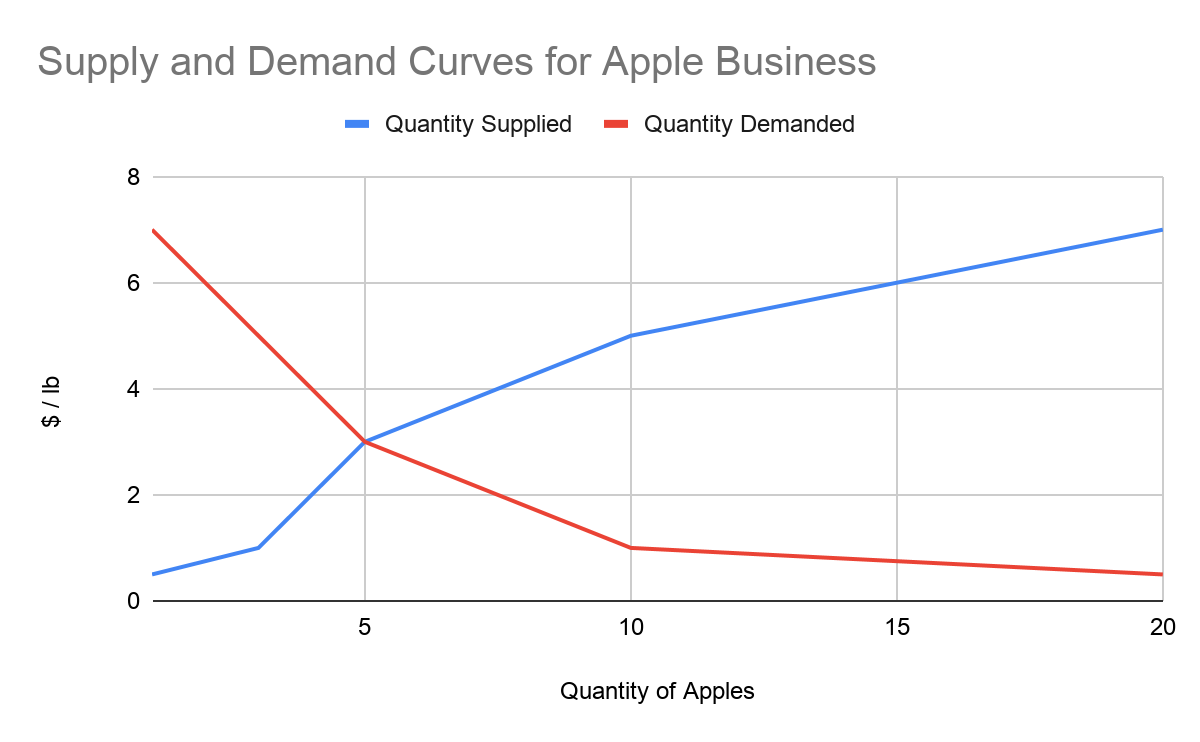

If we go back to our apple business example, imagine for the sake of simplicity that the quantity supplied is an exact inverse to the quantity demanded at the same price. In truth, the supply curve could be different based on other factors in the supply chain. If we were to create a supply curve and a demand curve on the same graph, we would get:

We can see that when the price is set to $3.00/lb, the consumers demand the same quantity that you as a business are willing to provide. This intersection of the supply and demand curves is called equilibrium. At equilibrium, the market is most efficient because the demand of the consumers matches the producers’ supply at a price both groups can agree on.

Any price that falls above equilibrium is considered an excess of supply, which creates a surplus. This means the producer will provide more than consumers want.

Any price that falls below equilibrium is an excess of demand, which creates a shortage. This means the producer provides less than what the consumers want. Surpluses and shortages are symptoms of an unhealthy economy.

Why Is Understanding Demand Important?

If you are an employee of a for-profit company, your business will want to make sure that it can meet the consumer’s demands in a sustainable way. It is particularly important for your business to set a price at equilibrium so that it can produce within its means while still meeting the consumer’s demand.

Depending on your role at the company, such as an accountant, you will want to make sure your price generates enough revenue to cover expenses and build a profit. If you work in marketing or sales, you may be more focused on other determinants of demand to generate more interest for your consumers.

Final Thoughts

The demand of the consumer is a force that cannot be taken for granted. Without proper knowledge of demand, businesses find themselves at risk of surpluses or shortages, which can have compounding negative effects.

If you plan to offer a competitive good or service, then you must monitor demand at all times.

- Glossary

- What Is Gross Monthly Income?

- What Is Management?

- What Is A Problem Statement?

- What Is Annual Net Income?

- What Is A Letter Of Transmittal?

- What Is Attrition?

- What Does White Collar Mean?

- What Does Blue Collar Mean?

- What Is Efficiency Vs Effectiveness?

- What Is A Dislocated Worker?

- What Is Human Resource (HR)?

- Thank You Letter Scholarships

- What Is Constructive Criticism?

- What Is A Quarter Life Crisis?

- What Is Imposter Syndrome?

- What Is Notes Payable?

- Types Of Communication

- Economic Demand

- Cost Benefit Analysis

- Collective Bargaining

- Key Performance Indicators

- What Is Gender Bias In A Job Description?

- What Is The Hidden Job Market?

- What Is The Difference Between A Job Vs. A Career?

- What Is A Prorated Salary?

- W9 Vs. 1099

- Double Declining Balance Method

- Divergent Vs Convergent Thinking

- Budgeting Process

- Types Of Intelligence

- What Is Bargaining Power?

- What Is Operating Capital?

- Difference Between Margin Vs Markup

- Participative Leadership

- Autocratic Leadership

- Authoratarian Leadership

- Situational Leadership

- Difference Between Generalist Vs Specialist

- Strategic Leadership

- Competitive Strategies

- Equity Vs Equality

- What Is Marginalization?

- Colleague Vs Coworker

- What Is The Glass Ceiling?

- What Are Guilty Pleasures?

- Emotion Wheel

- Nepotism In The Workplace

- Sustainable Competitive Advantage

- Organizational Development

- Communication Styles

- Contingent Workers

- Passive Vs Non Passive Income

- Choose A Career

- Formulas

- APR Formula

- Total Variable Cost Formula

- How to Calculate Probability

- How To Find A Percentile

- How To Calculate Weighted Average

- What Is The Sample Mean?

- Hot To Calculate Growth Rate

- Hot To Calculate Inflation Rate

- How To Calculate Marginal Utility

- How To Average Percentages

- Calculate Debt To Asset Ratio

- How To Calculate Percent Yield

- Fixed Cost Formula

- How To Calculate Interest

- How To Calculate Earnings Per Share

- How To Calculate Retained Earnings

- How To Calculate Adjusted Gross Income

- How To Calculate Consumer Price Index

- How To Calculate Cost Of Goods Sold

- How To Calculate Correlation

- How To Calculate Confidence Interval

- How To Calculate Consumer Surplus

- How To Calculate Debt To Income Ratio

- How To Calculate Depreciation

- How To Calculate Elasticity Of Demand

- How To Calculate Equity

- How To Calculate Full Time Equivalent

- How To Calculate Gross Profit Percentage

- How To Calculate Margin Of Error

- How To Calculate Opportunity Cost

- How To Calculate Operating Cash Flow

- How To Calculate Operating Income

- How To Calculate Odds

- How To Calculate Percent Change

- How To Calculate Z Score

- Cost Of Capital Formula

- How To Calculate Time And A Half

- Types Of Variables

Author

Conor McMahon is a writer for Zippia, with previous experience in the nonprofit, customer service and technical support industries. He has a degree in Music Industry from Northeastern University and in his free time he plays guitar with his friends. Conor enjoys creative writing between his work doing professional content creation and technical documentation.